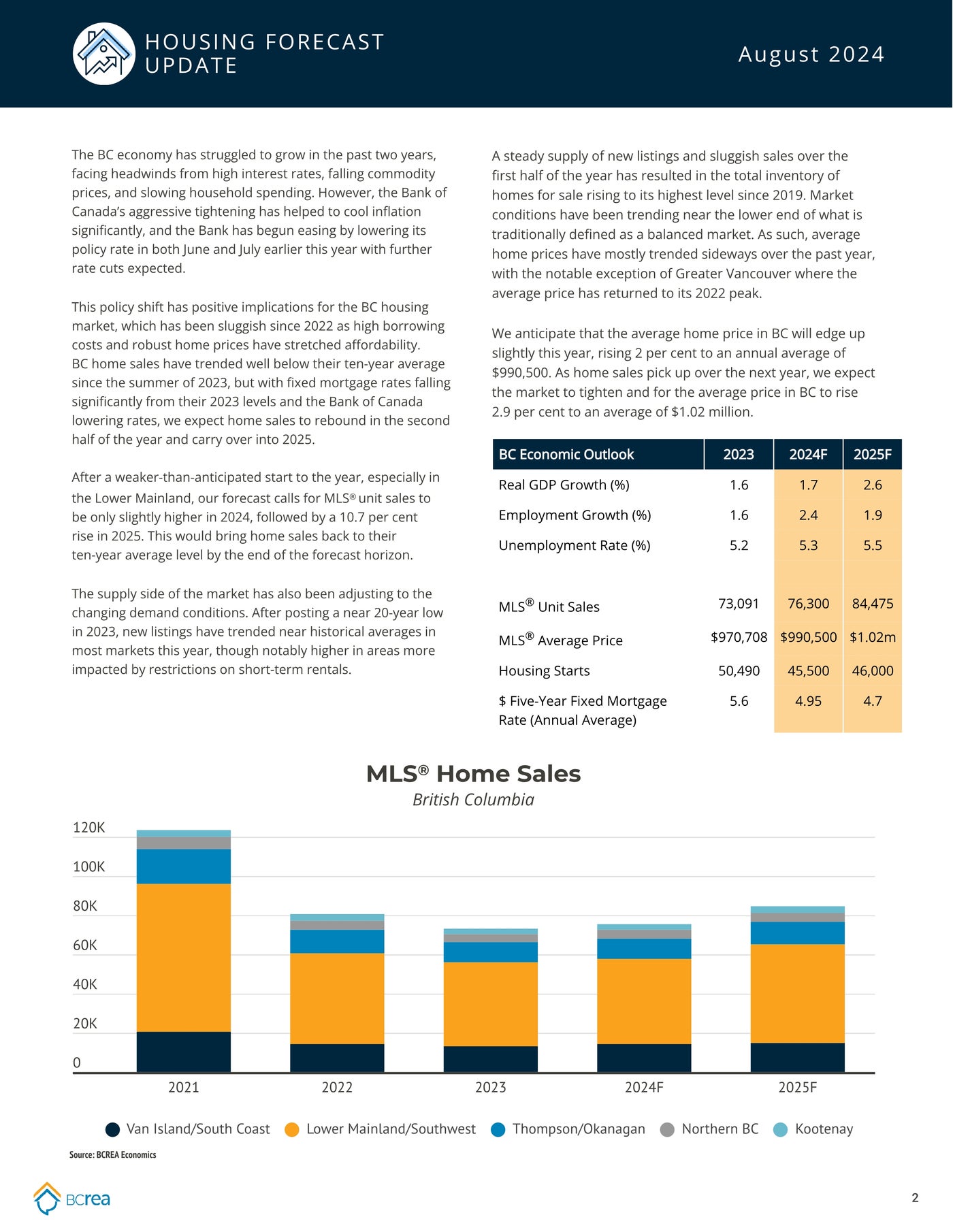

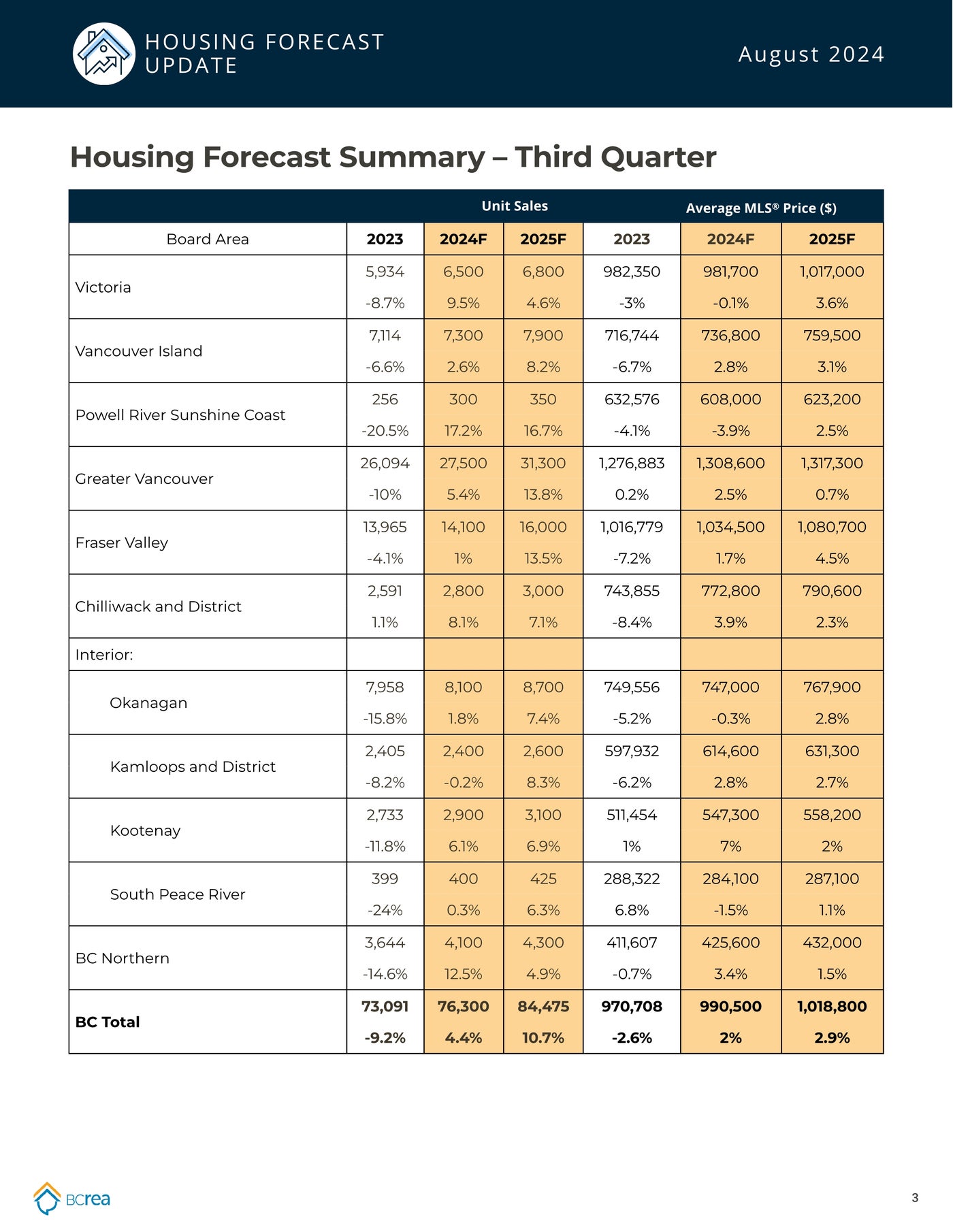

August 2024 Statistics for Single Family Dwellings in the Cowichan Valley

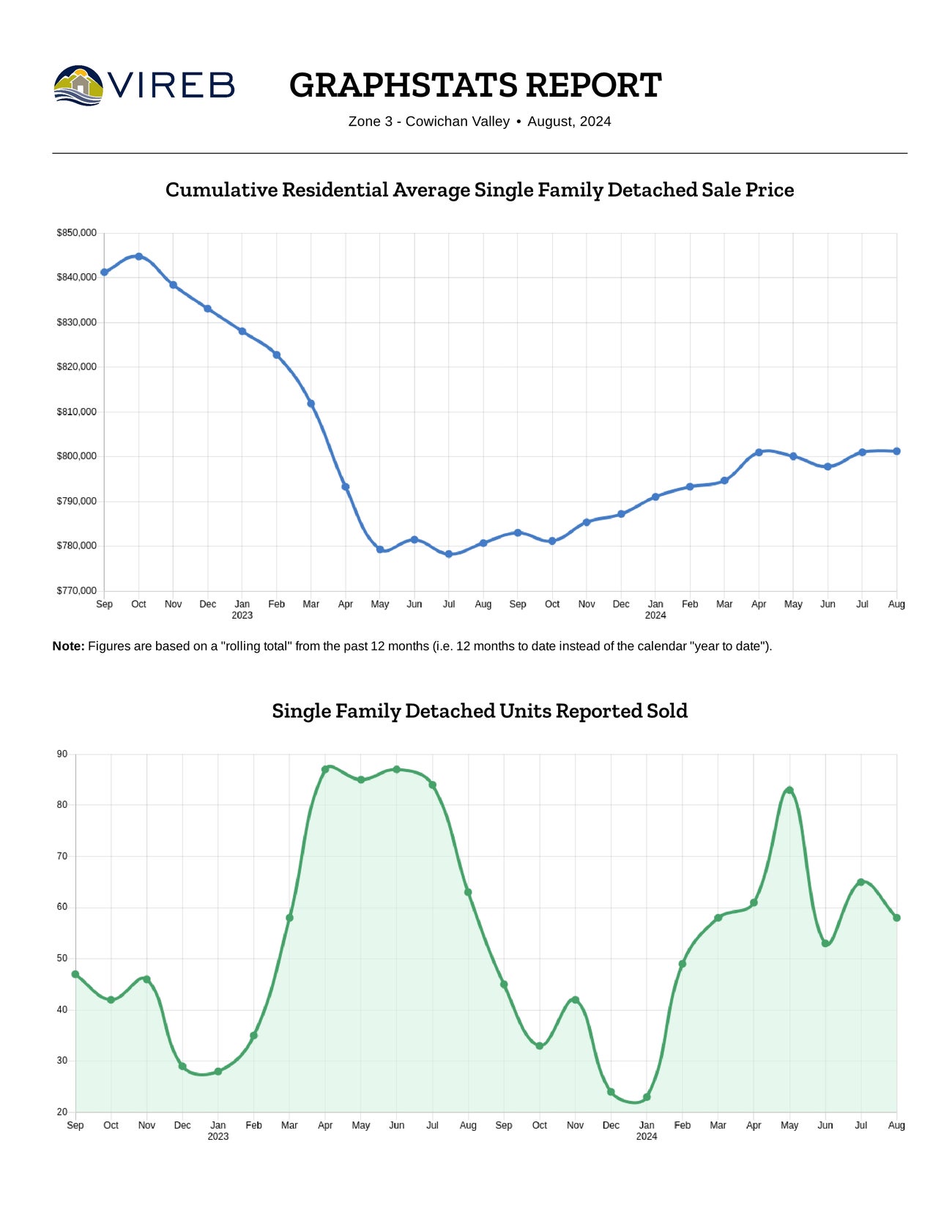

August saw a total of 58 single-family homes sold in the Cowichan Valley, down from the 63 that sold in August of last year, and down from the 65 in the preceding month of July. There were 101 single-family homes listed on the market in August 2024 compared to 66 last year, up 53%. There were 1,251 sales in our valley over the past 12 months representing a 10% increase in comparison to the 1,136 sales in the 12 months ending in August of last year. The 12 months to date average selling price of a home is +2.6%.

Average prices for single-family residential homes in August 2024 were at $803,666, virtually the same as $801,089 in August 2023, and as July’s average of $802,451. The median price of a single-family home in the Cowichan Valley for the 12 months to date ending in August 2024 was $785,000.

In August, the active inventory of single-family homes on the market in the Cowichan Valley was 316, up from the 183 homes at the end of August 2023.

We had a 7.2-month supply of single-family homes on the market last month, while August 2023 had a 4.4-month supply. The average days to sell a single-family home in August was 54 days, up from 34 days last August.

Condos and Townhouse

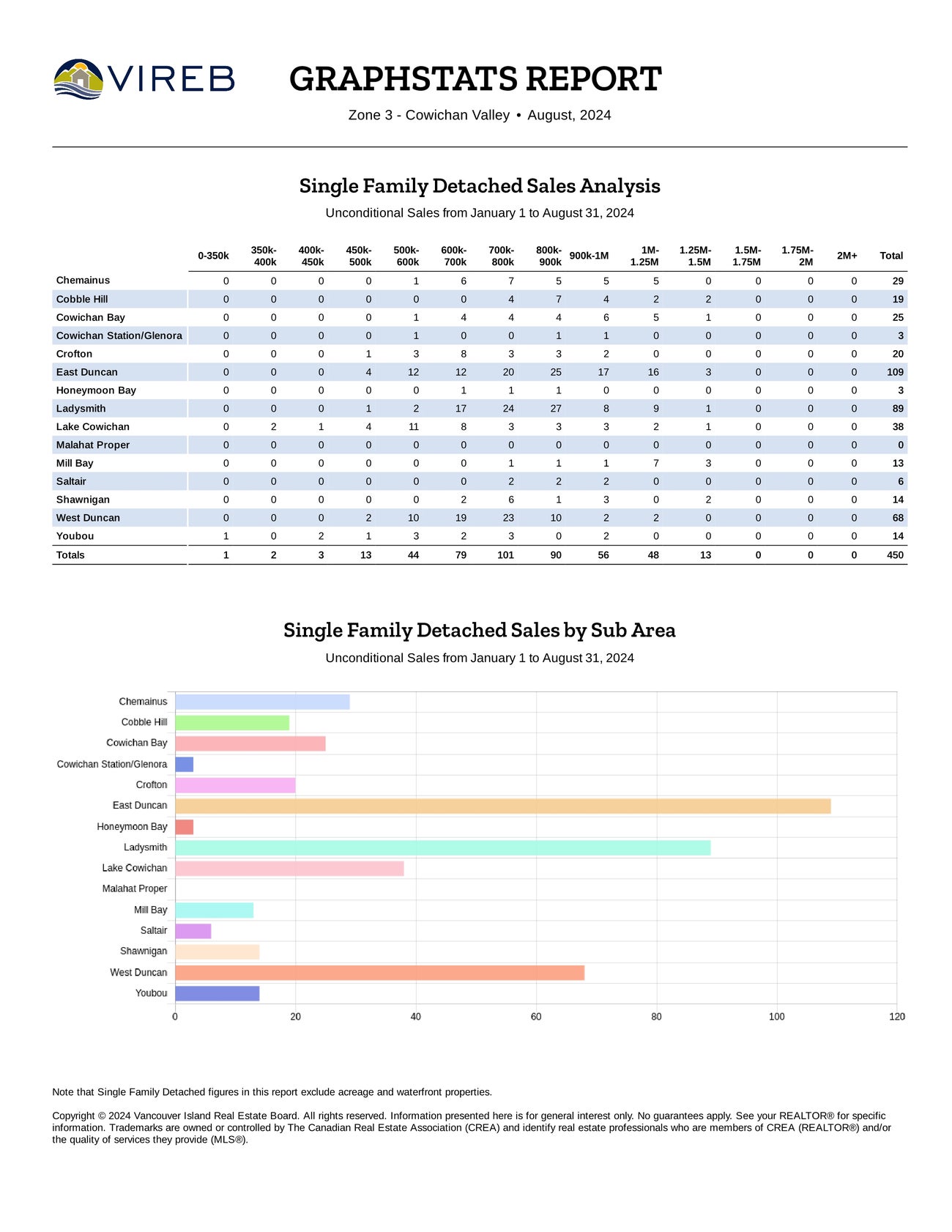

Condominium apartment sales in August saw 6 units sold, down from 15 sales in the previous month of July, and down from the 12 units that sold last August. Condo apartments in the valley saw the average price for the 12 months ending in August 2024 at $353,191, up 6% for the same period as last year, $334,273.

The inventory of Townhomes on the market saw 12 sales in August, up from the 11 that sold in the month of July, and down from the 15 sold last August, a 20% decrease. Townhomes in the valley saw the average price for the 12 months to date ending in August at $447,857, up 10% from $405,928 for the same period last year.

If you would like to see my current listings, please click here.

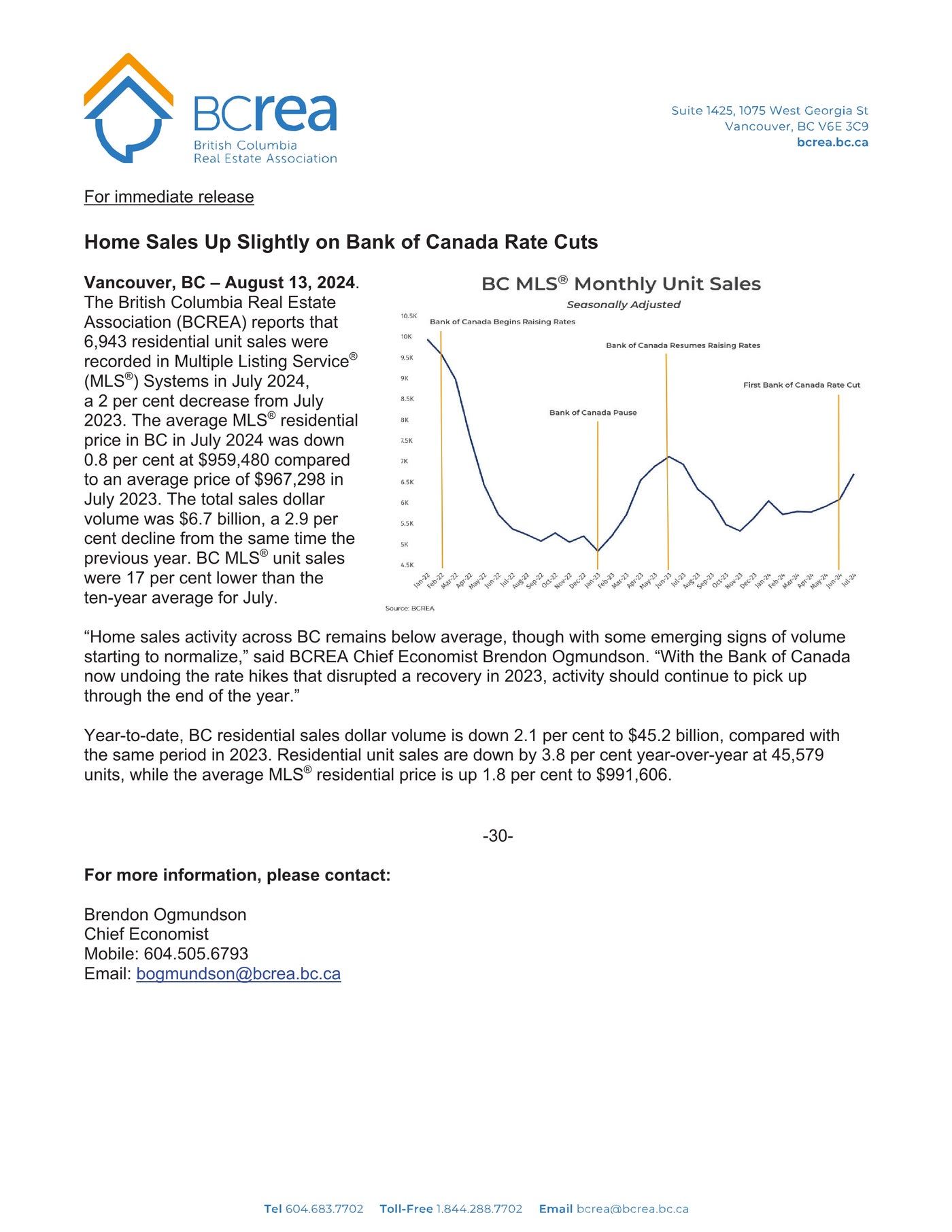

Ottawa, ON August 15, 2024 - While there were early signs of renewed momentum in June following the Bank of Canada’s first interest rate cut since 2020, activity in Canada’s housing market took a pause in July.

Home sales activity recorded over Canadian MLS® Systems edged back by 0.7% on a month-over-month basis in July 2024, giving back a small portion of June’s post-first rate cut gain. (Chart A)

Home sales activity recorded over Canadian MLS® Systems edged back by 0.7% on a month-over-month basis in July 2024, giving back a small portion of June’s post-first rate cut gain. (Chart A)

“With another rate cut announced on July 24, we’ve now seen two rate cuts in a row, and the expected pace of future policy easing has steepened considerably, with markets now anticipating rate cuts at every remaining Bank of Canada decision this year,” said Shaun Cathcart, CREA’s Senior Economist. “Combine that with a record amount of demand waiting in the wings, and the forecast for a rekindling of Canadian housing activity going into 2025 has just gone from a layup to a slam dunk.”

Highlights:

• National home sales edged back 0.7% month-over-month in July.

• Actual (not seasonally adjusted) monthly activity came in 4.8% above July 2023.

• The number of newly listed properties ticked up 0.9% month-over-month.

• The MLS® Home Price Index (HPI) edged up 0.2% month-over-month but was down 3.9% year-over-year.

• The actual (not seasonally adjusted) national average sale price was almost unchanged (-0.2%) on a year-over-year basis in July.

• National home sales edged back 0.7% month-over-month in July.

• Actual (not seasonally adjusted) monthly activity came in 4.8% above July 2023.

• The number of newly listed properties ticked up 0.9% month-over-month.

• The MLS® Home Price Index (HPI) edged up 0.2% month-over-month but was down 3.9% year-over-year.

• The actual (not seasonally adjusted) national average sale price was almost unchanged (-0.2%) on a year-over-year basis in July.

Monthly changes in sales activity were generally small amongst the larger centres in July. Interestingly, declines in Calgary and the Greater Toronto Area were mostly offset by gains in Edmonton and Hamilton-Burlington.

As of the end of July 2024, there were about 183,450 properties listed for sale on all Canadian MLS® Systems, up 22.7% from a year earlier but still about 10% below historical averages of more than 200,000 for this time of the year.

New listings posted a slight 0.9% month-over-month increase in July. The national increase was led by a much-needed boost in new supply in Calgary.

New listings posted a slight 0.9% month-over-month increase in July. The national increase was led by a much-needed boost in new supply in Calgary.

With new listings up slightly and sales down slightly, in July, the national sales-to-new listings ratio eased back to 52.7% compared to 53.5% in June. The long-term average for the national sales-to-new listings ratio is 55%, with a sales-to- new listings ratio between 45% and 65% generally consistent with balanced housing market conditions.

“While it wasn’t apparent in the July housing data from across Canada, the stage is increasingly being set for the return of a more active housing market,” said James Mabey, Chair of CREA. “At this point, many markets have a healthier amount of choice for buyers than has been the case in recent years, but the days of the slower and more relaxed house hunting experience may be somewhat numbered. If you’re hoping to get into the market ahead of the pack, contact a REALTOR® in your area today.”

There were 4.2 months of inventory on a national basis at the end of July 2024, unchanged from the end of June. The long-term average is about five months of inventory.

The National Composite MLS® Home Price Index (HPI) edged up 0.2% from June to July. While a small increase, it was slightly larger than the June increase, making it just the second, and the largest, gain in the last year.

While prices were up slightly at the national level, they were held back by reduced activity in the largest and most expensive British Columbia and Ontario markets. Regionally, prices are rising in a growing number of markets – a majority at this point.

The non-seasonally adjusted National Composite MLS® HPI stood 3.9% below July 2023. This mostly reflects how prices took off last April, May, June, and July – something that was not repeated over that same period in 2024. It’s mostly likely that year-over-year comparisons will improve from this point on.

The actual (not seasonally adjusted) national average home price was $667,317 in July 2024, almost unchanged (-0.2%) from July 2023.

Bank of Canada reduces policy rate by 25 basis points to 4¼%

FOR IMMEDIATE RELEASE

Media Relations

Ottawa, Ontario

September 4, 2024

The Bank of Canada today reduced its target for the overnight rate to 4¼%, with the Bank Rate at 4½% and the deposit rate at 4¼%. The Bank is continuing its policy of balance sheet normalization.

The global economy expanded by about 2½% in the second quarter, consistent with projections in the Bank’s July Monetary Policy Report (MPR). In the United States, economic growth was stronger than expected, led by consumption, but the labour market has slowed. Euro-area growth has been boosted by tourism and other services, while manufacturing has been soft. Inflation in both regions continues to moderate. In China, weak domestic demand weighed on economic growth. Global financial conditions have eased further since July, with declines in bond yields. The Canadian dollar has appreciated modestly, largely reflecting a lower US dollar. Oil prices are lower than assumed in the July MPR.

In Canada, the economy grew by 2.1% in the second quarter, led by government spending and business investment. This was slightly stronger than forecast in July, but preliminary indicators suggest that economic activity was soft through June and July. The labour market continues to slow, with little change in employment in recent months. Wage growth, however, remains elevated relative to productivity.

As expected, inflation slowed further to 2.5% in July. The Bank’s preferred measures of core inflation averaged around 2 ½% and the share of components of the consumer price index growing above 3% is roughly at its historical norm. High shelter price inflation is still the biggest contributor to total inflation but is starting to slow. Inflation also remains elevated in some other services.

With continued easing in broad inflationary pressures, Governing Council decided to reduce the policy interest rate by a further 25 basis points. Excess supply in the economy continues to put downward pressure on inflation, while price increases in shelter and some other services are holding inflation up. Governing Council is carefully assessing these opposing forces on inflation. Monetary policy decisions will be guided by incoming information and our assessment of their implications for the inflation outlook. The Bank remains resolute in its commitment to restoring price stability for Canadians.

Information note

The next scheduled date for announcing the overnight rate target is October 23, 2024. The Bank will publish its next full outlook for the economy and inflation, including risks to the projection, in the MPR at the same time.

The next scheduled date for announcing the overnight rate target is October 23, 2024. The Bank will publish its next full outlook for the economy and inflation, including risks to the projection, in the MPR at the same time.